Explaining the IRS – Personal Income Tax (IRS) tax bill IRS

The tax bill is issued until the end of July and normally payable until the end of August. Below you can see a sample of the tax bill in Portuguese called Nota de Liquidação, and what this refers to.

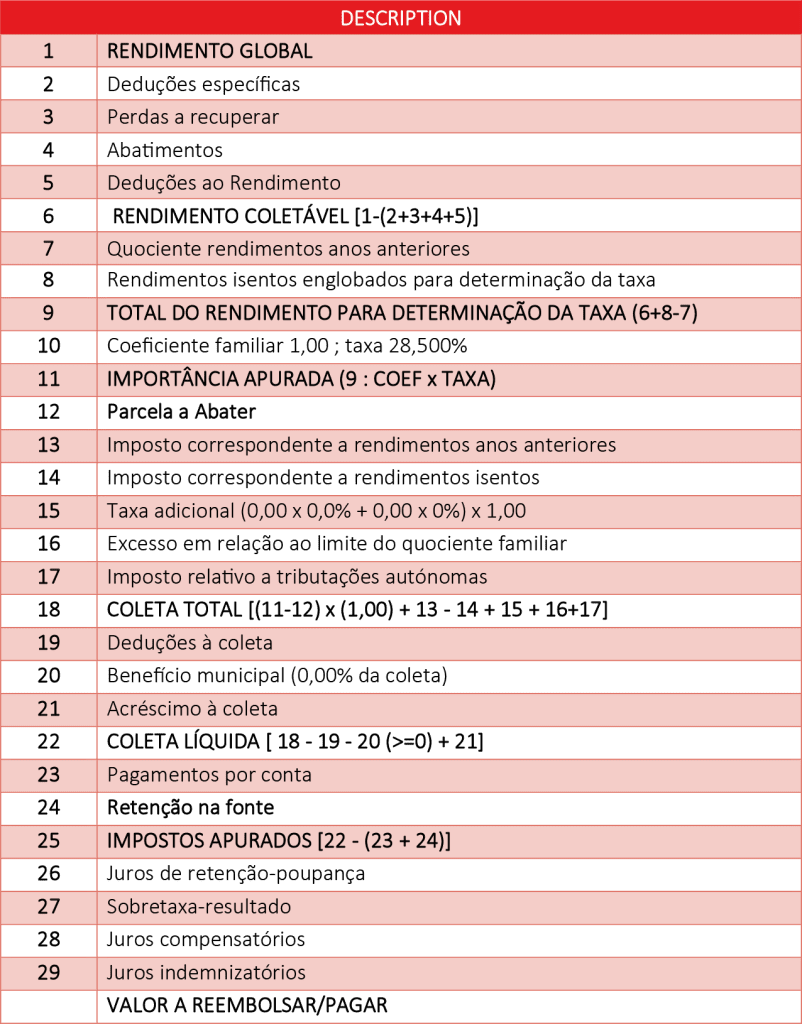

The IRS tax bill or settlement note (Nota de liquidação) displays the calculations made by the Tax Authorities, to determine what IRS do you have to pay or receive.

The tax bill is sent to the taxpayer address, or to his fiscal representative. It may also be sent via email, for those who have signed up, through ViaCTT, an electronic mailbox. Please note that if the taxpayer has a registered activity at the tax office (self-employment) then

As a rule, those who are entitled to a tax refund and have indicated the IBAN in the IRS declaration receive the transfer from the Tax Auhtorities, even before the settlement note (Nota de Liquidação) is sent. For those who will have to pay tax, this document contains the data that allows you to make the payment. Normally the payment is due until the end of August.

The tax refund is no more than the return to the taxpayer of the IRS retained on source in excess during the previous tax year, either through withholding taxes or payments on account. To find out how much it advanced to the State in 2020, see installments 23 (payments on account) and 24 (withholding taxes). These will be deducted from the amount that it was supposed to deliver, and which is indicated in portion 22, relating to the net collection. If there is any money left over, there is a refund. If advance payments are not sufficient, there is still tax to be paid.

Overall income

Sum of all income earned by the taxpayer, for example, with wages or services rendered. Please note that if you are a service provider, not all the income shows here, just a percentage. For instance if you provide services, the income is 10.000€ but only the taxable income is shown here and this varies depending of your activity.

Specific deductions

This refers to tax deductions and it’s taken from the overall income. It can be fixed, as happens to most employees, or may depend on the expenses incurred, as happens to landlords, if they opt for the aggregation of all income.

Losses to be recovered

Investors with negative results, for example, from the sale of shares, or landlords with more expenses than income, may try to recover the loss in the following year’s IRS.

Taxable income

This is the income that determines the tax rate to be applied. It corresponds to the difference between gross income and specific deductions.

Exempt income included for rate determination

This refers to income that is tax exempt, for instance the income of those who work for diplomatic missions or the income from pensions for Non Habitual residents (under the law previous to 31-03-2020). This income is exempt, however is considered to determine the tax rate applicable to other income that pays tax.

Family coefficient

Divide income by the number of taxpayers. For single, widowed or divorced persons, the coefficient “1” is applied; in the case of married or de facto united persons who opt for the joint declaration, the income is divided by “2”.

Calculated amount and installment to be deducted

They vary depending on the taxpayer’s income: the higher, the more aggravated the rate.

Autonomous taxation

The taxpayer can opt for autonomous taxation of some income. Instead of these being added to the others to determine the rate to be applied, a single and definitive rate is charged. This could be the case of capital or rental income, where the income is taxed normally at 28%.

Tax before deductions

Tax that the taxpayer would have to pay if there were no deductions or withholding tax during the previous year.

Tax deductions

The amount of expenses that the tax authorities take into account (health or education, for example) is subtracted from the tax payable. These deductions are based on the invoices you collected with your fiscal number, and have been validated on the e-fatura platform until February 25th.

Municipal benefit

Some municipalities choose to deliver to residents part, or all, of the income tax to which they are entitled. The percentage is decided annually and can reach 5 percent.

Additional tax

When the taxpayer withdraws amounts invested in investments with tax benefits, for example, PPR, outside the foreseen conditions, he is subject to a penalty (he must return the tax benefits enjoyed, plus 10% for each year). It is added to the tax payable.

Net tax

Amount that the taxpayer actually has to pay, after all deductions have been considered and before considering the tax already paid or withhold.

Payments on account

Self-employed workers who have not made sufficient withholding taxes in previous years may be required to make upfront tax payments based on what they earned. These amounts are deducted from the tax payable.

Withholding taxes

This is the tax withheld when income was earned. In the final accounts, it is subtracted from the tax payable.

Calculated tax

Tax payable or refundable if there are no more calculation installments.

Interest

When the taxpayer is entitled to a tax refund for having been charged more tax in the previous year, the tax authorities may pay a small interest.

Tax to be paid or received

It corresponds to the amount that the taxpayer will pay of IRS or the tax redund that he will now receive.